Capital Gains Tax India 2025 – Complete Guide for Investors

4/10/20252 min read

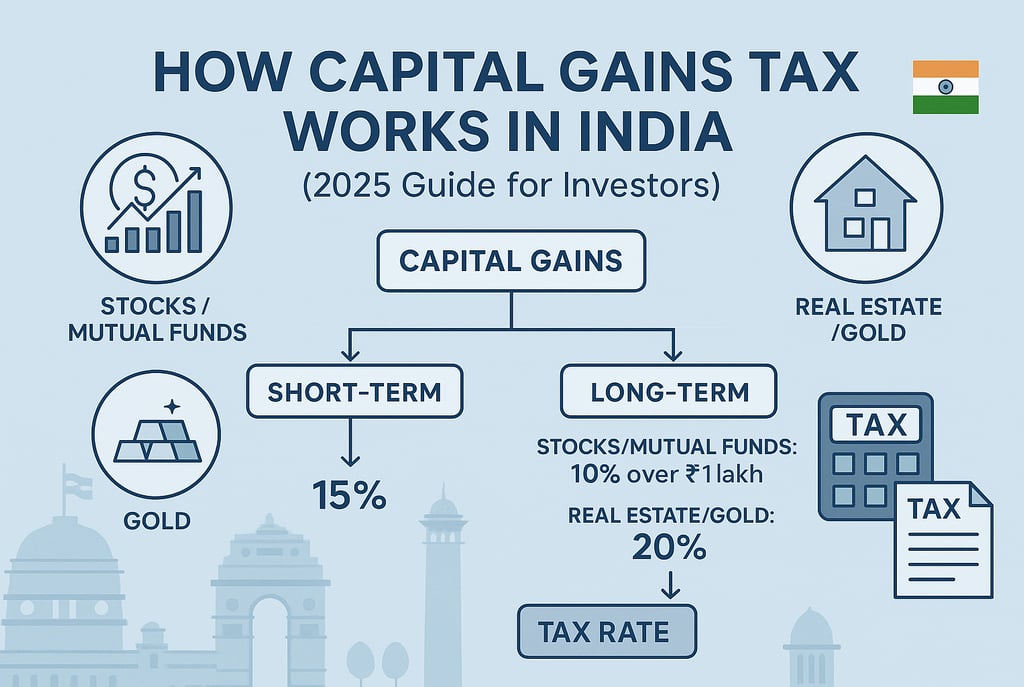

How Capital Gains Tax Works in India (2025 Guide for Investors)

Understanding how capital gains tax works is essential for any investor in India. Whether you’re investing in stocks, mutual funds, real estate, or gold, the profits you earn may be subject to taxation. In 2025, with financial markets becoming more dynamic and the government enhancing tax transparency, investors must stay informed to avoid surprises and plan smartly.

What Is Capital Gains Tax?

Capital gains tax is a levy on the profit earned from the sale of a capital asset. These assets can include:

Stocks and equity mutual funds

Real estate

Bonds and debt mutual funds

Gold, ETFs, and other investments

The tax applies only when the asset is sold, and the gain is realized. The gains are classified based on the holding period of the asset—short-term or long-term.

Types of Capital Gains in India (2025)

1. Short-Term Capital Gains (STCG):

For stocks and equity-oriented funds: Held for less than 12 months

Tax Rate: 15%

STCG is added to your total income if the security is not listed (e.g., unlisted shares).

2. Long-Term Capital Gains (LTCG):

For stocks and equity-oriented mutual funds: Held for more than 12 months

Tax Rate: 10% on gains above ₹1 lakh (without indexation)

For real estate, debt funds, and gold: Held for more than 36 months

Tax Rate: 20% with indexation

Indexation adjusts the purchase price for inflation, reducing taxable gains and lowering the tax liability.

Capital Gains Tax on Various Assets

Stocks and Equity Mutual Funds

STCG: 15% (if sold within 1 year)

LTCG: 10% (after 1 year, if gains exceed ₹1 lakh annually)

Real Estate

STCG: Taxed as per individual slab (held <2 years)

LTCG: 20% with indexation (held >2 years)

Gold and Debt Funds

STCG: Added to income and taxed as per slab

LTCG: 20% with indexation after 36 months

How to Save Capital Gains Tax (Legally)

Invest in Capital Gains Bonds (Section 54EC)

Applicable for real estate LTCG

Invest up to ₹50 lakh in 54EC bonds (NHAI, REC)

Lock-in: 5 years

Use Section 54 for Real Estate Reinvestment

Reinvest sale proceeds in another residential property within 2 years (or construct within 3)

Set Off Against Capital Losses

Offset gains against prior short or long-term capital losses

Tax Harvesting

Book profits up to ₹1 lakh annually on equity to reset acquisition price and reduce future LTCG

How to Calculate Capital Gains Tax

Capital Gains = Sale Price – (Purchase Price + Transfer Costs + Improvement Costs)

For LTCG (except equity), apply indexation to purchase price using the Cost Inflation Index (CII).

Things to Keep in Mind in 2025

Digital reporting of capital gains is now integrated with income tax e-filing.

Mutual fund taxation now applies a uniform treatment post-April 2023 (debt funds no longer get indexation unless grandfathered).

Intraday profits are not capital gains; they are business income and taxed at slab rate.

Final Thoughts

Capital gains tax plays a crucial role in shaping your investment returns. With proper planning, you can reduce tax outgo while staying compliant. Whether it’s investing in tax-saving bonds, using the right holding period, or utilizing losses effectively—being aware is half the battle won.

At One Solution, we help investors manage portfolios efficiently, identify tax-saving opportunities, and optimize capital gain outcomes. Book your free portfolio review today.

Related Blogs:

About One Solution

Quick Links

Contact Info

One Solution — Your trusted partner for financial success.

📍 F17, Grand Plaza, Paltan Bazar

Guwahati, Kamrup (M), Assam

India, Pin: 781008

📞 9650072280

© 2025 One Solution. All Rights Reserved.