ELSS vs PPF vs NPS – Which Tax Saving Investment Is Best for You in 2025?

4/5/20252 min read

ELSS vs PPF vs NPS – Which Tax Saving Investment Is Best for You in 2025?

Choosing the right tax-saving investment can be confusing, especially with so many options under Section 80C. Among the most popular are ELSS (Equity Linked Savings Scheme), PPF (Public Provident Fund), and NPS (National Pension System) — each offering tax benefits but differing significantly in terms of returns, lock-in, risk, and liquidity.

This detailed comparison will help you decide which one aligns best with your income, investment goals, and risk profile in 2025.

1. Investment Objective & Type

ELSS: Market-linked mutual fund with equity exposure; goal is long-term wealth creation.

PPF: Government-backed savings scheme; focused on safe, long-term capital protection.

NPS: Retirement-focused hybrid instrument with equity + debt mix; goal is pension accumulation.

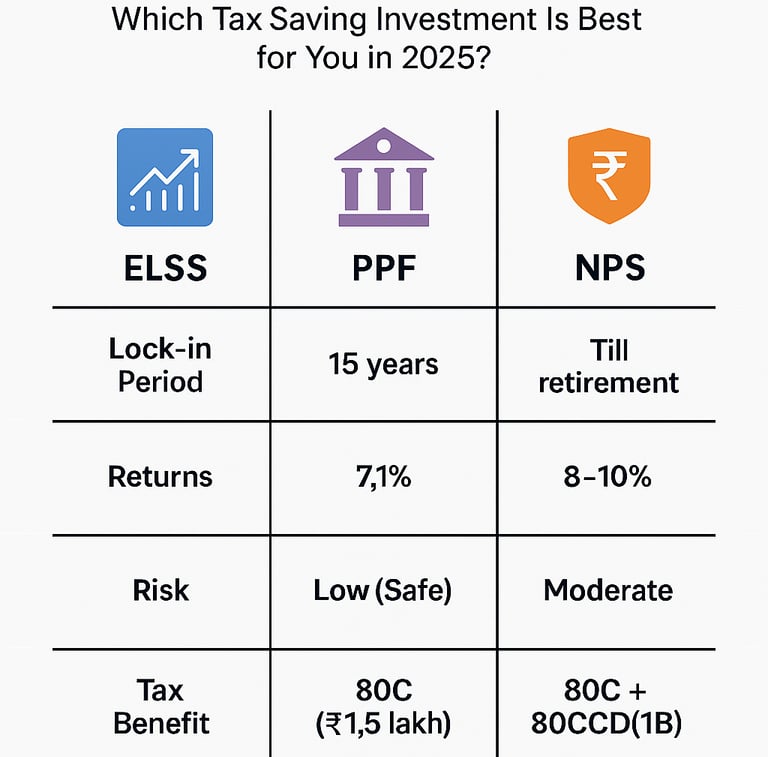

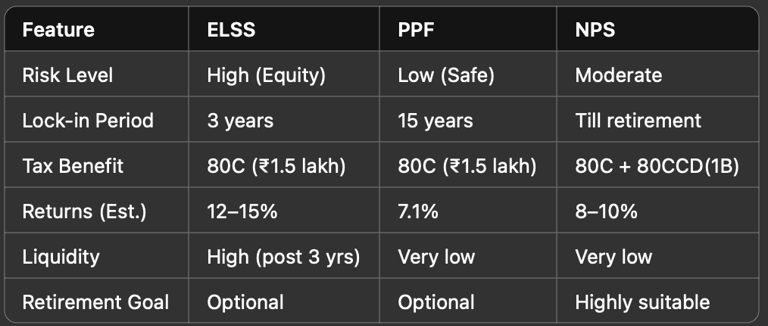

2. Tax Benefits

ELSS: Deduction under Section 80C up to ₹1.5 lakh; returns taxed as LTCG (10% on gains > ₹1 lakh/year).

PPF: Full EEE benefit – principal, interest, and maturity amount are tax-free.

NPS: Deduction up to ₹2 lakh (₹1.5 lakh under 80C + ₹50,000 under 80CCD(1B)); 60% corpus at maturity is tax-free.

3. Lock-in Period

ELSS: 3 years (shortest among 80C options).

PPF: 15 years (with partial withdrawal after 7 years).

NPS: Locked until retirement (60 years); partial withdrawal allowed after 3 years under specific conditions.

4. Returns & Risk Profile

ELSS: High return potential (~12–15%) but comes with equity market risk.

PPF: Fixed returns (~7.1% currently); safest option, backed by the government.

NPS: Moderate to high returns (~8–10%) depending on equity allocation; low cost structure.

5. Liquidity & Withdrawal

ELSS: Full withdrawal after 3 years.

PPF: Partial withdrawal from year 7; full withdrawal only after 15 years.

NPS: Limited withdrawal options; 60% can be withdrawn tax-free at retirement, 40% must be used for annuity.

6. Suitability

Choose ELSS if you are comfortable with market-linked volatility and want high long-term returns with the lowest lock-in.

Choose PPF if you are risk-averse, prefer stable returns, and want a secure, long-term savings option.

Choose NPS if your goal is retirement planning and you’re looking for an additional ₹50,000 tax deduction over 80C.

Quick Comparison Table

Final Thoughts

There is no “one size fits all” in tax planning. Each of these instruments serves a unique purpose.

ELSS is best for aggressive investors targeting growth.

PPF suits conservative savers building secure, tax-free wealth.

NPS is tailor-made for retirement with an extra tax-saving edge.

The ideal strategy? Combine all three based on your financial goals, income level, and risk profile.

Need help structuring your 2025 tax-saving investments? One Solution offers personalized advisory services, portfolio tracking, and support to help you choose the right combination — tax-efficient and goal-aligned.

Related Blogs:

Section 80C Explained – Maximize Your Deduction

How to Build a Tax-Efficient Portfolio in 2025

About One Solution

Quick Links

Contact Info

One Solution — Your trusted partner for financial success.

📍 F17, Grand Plaza, Paltan Bazar

Guwahati, Kamrup (M), Assam

India, Pin: 781008

📞 9650072280

© 2025 One Solution. All Rights Reserved.